Your Savings Game Plan

Your step-by-step priority ladder from $0 to retirement-ready

When My Savings Game Plan Finally Clicked

For most of my teaching career, I didn't have a savings game plan. I didn't even have a plan. I had a paycheck, bills, and whatever was left over — which usually wasn't much.

That changed when I went down the financial literacy rabbit hole. I started reading, listening to podcasts, and interacting in online communities. The more I learned, the more I realized what I needed to do. It wasn't one single moment — it was a hundred small lightbulbs going off at once.

And once I had the plan? I attacked it from both sides. I ramped up my income with side hustles and summer work (the strategies I shared in Module 3). On the other side, I cut my expenses as low as I possibly could — including moving into a studio apartment (Module 1) and continuing to drive my old paid-off Honda Civic (Module 3).

The Question Every Teacher Asks: "How Much Should I Actually Save?"

You've learned about the 30% income gap. You understand 403(b) and 457(b) accounts. You've found money in your budget. Now comes the million-dollar question:

"Okay Coach, HOW MUCH do I need to save each month?"

Financial experts recommend saving 15-20% of your gross income for retirement. But here's what's unique about teachers:

That means you need another 5-10% going into your 403(b) or 457(b) to hit the target — your pension contribution already covers roughly 5-8% — but your age matters just as much as your salary.

If you're in your 20s or 30s, time is your superpower — even 5% on top of your pension puts compound interest to work for decades. In your 40s, you'll want to push toward 10-15% to stay on track. And if you're 50+? This is your catch-up decade. Consider being as aggressive as your budget allows — 15-20%+ beyond your pension. I didn't start until 52 and went all in. It's not too late, but the urgency is real.

Here's something a lot of teachers don't realize: you're already saving for retirement. Look at your paycheck stub — there's a pension deduction coming out every single pay period, usually around 7-10% of your salary. Your district also contributes to the pension system on your behalf — but here's the important part: that employer contribution goes into the overall pension fund, not into a personal account with your name on it. If you leave teaching before vesting and take a refund, you typically only get back your own contributions. Even after vesting, withdrawing your contributions means forfeiting the employer contributions and your future pension benefit. That said, as long as you stay in the system and vest, those combined contributions are what build your pension benefit over time.

Why does this matter? Because when I say you need to save an additional 5-10% in your 403(b) or 457(b), you're not starting from zero. You're building on top of a foundation that's already there. That makes the target a lot more doable than it sounds.

Real Numbers for Real Teachers

| Your Salary | Pension (≈10%) | Career Stage | Your Target | Monthly Amount |

|---|---|---|---|---|

| $50,000 | $5,000/yr | Early (20s-30s) | 5-10% | $208-$417/mo |

| $70,000 | $7,000/yr | Mid (40s) | 10-15% | $583-$875/mo |

| $90,000 | $9,000/yr | Late (50+) | 15-20%+ | $1,125-$1,500/mo |

← Scroll to see full table →

*Pension (≈10%) reflects the approximate amount already deducted from your paycheck for your state pension — you're already saving for retirement.

Knowing how much to save each month is step one — but how do you know if you're actually on track? These checkpoints show where your balance should be at each stage of your career, based on YOUR pension and YOUR target retirement age.

How these checkpoints work: Assume you begin saving around age 25 and contribute consistently, assume an average 7% annual return, and calculated backward from your personal nest egg target above. Earlier checkpoints show smaller amounts because your remaining years of contributions and compound growth fill the gap.

Behind the target, or started later than 25? That’s okay — catch-up contributions (starting at age 50) and SECURE 2.0 super catch-up (ages 60–63) exist for exactly this reason. The 457(b) is also available to accelerate savings in your final working years. Use the calculators page to build a plan tailored to your timeline.

For reference: Fidelity’s general retirement guideline suggests saving 1x your salary by 30, 3x by 40, 6x by 50, and 8–10x by 60. Those benchmarks are designed for workers without pensions who need to fund 100% of retirement from savings. Teachers with pensions need less — the targets above are adjusted to your specific gap.

Hypothetical illustration for educational purposes only. Assumes consistent saving from age 25, 7% average annual return, 85% income replacement need, and 4% withdrawal rate. Does not account for inflation, taxes, healthcare costs, or longer life expectancy — many educators choose to aim higher for additional flexibility. Your actual target depends on your state pension formula, Social Security eligibility, and expected retirement expenses. Not personalized financial advice.

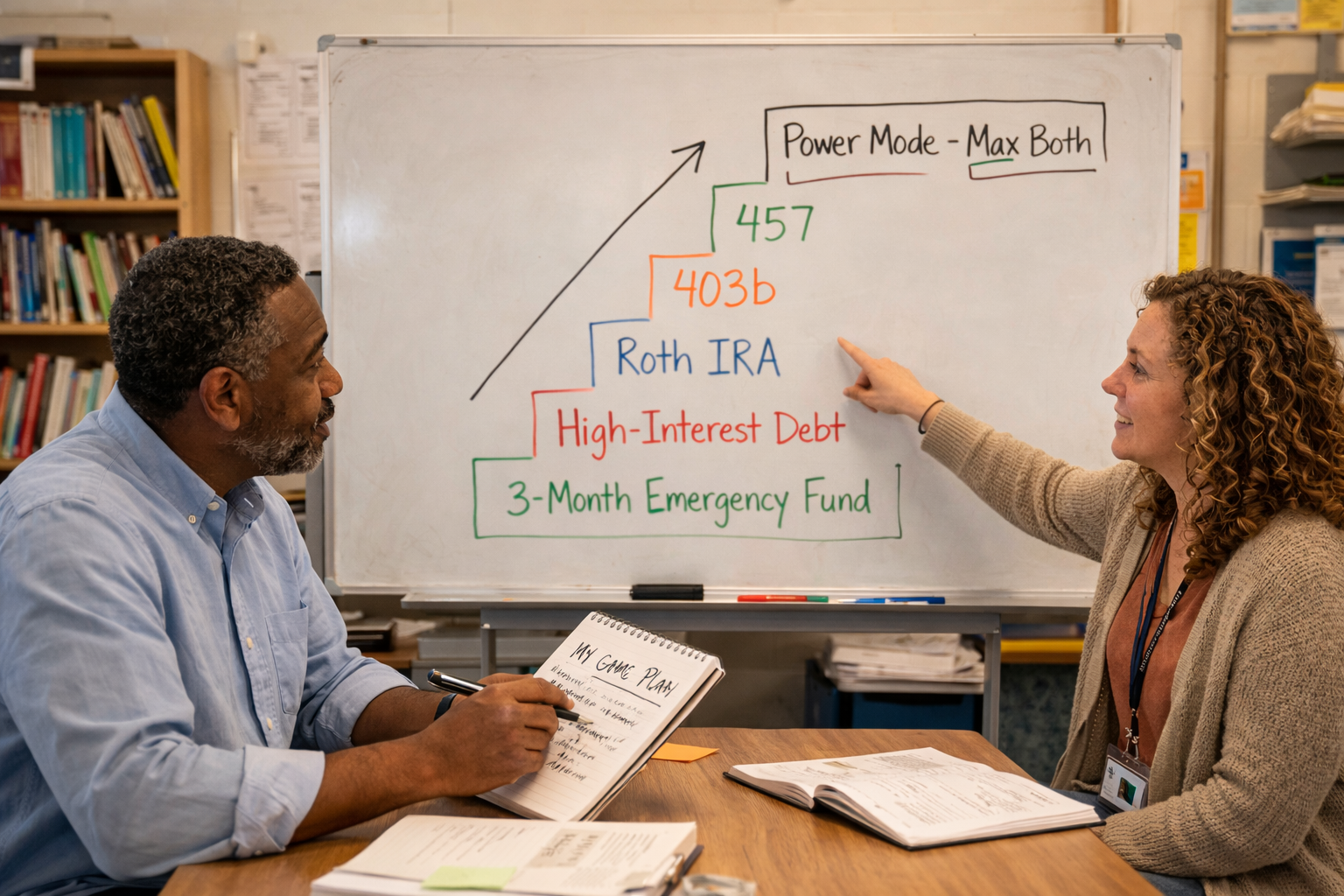

The Savings Priority Ladder: What to Do in What Order

This is where most teachers get stuck. You have limited money. Multiple goals. What comes first?

Here's the order that works for most teachers. Each step builds the foundation for the next — so it's worth working through them in sequence.

Better investment choices, no annuity traps, flexible access to contributions. Many teachers open theirs with low-cost providers like Fidelity or Vanguard (mentioned as educational examples, not endorsements) and invest in low-cost index funds. Many educators choose to max this before adding to the 403(b).

Over the income limit? Skip to Step 4.

Note: SECURE 2.0 super catch-up does not apply to IRAs

2026 income limits:

Single filers: phase out $153,000–$168,000

Married filing jointly: phase out $242,000–$252,000

See Module 6 for the complete strategy.

$4,400 individual / $8,750 family

Ages 55+: +$1,000 catch-up

Note: SECURE 2.0 super catch-up does not apply to HSAs

$24,500 base

Ages 50–59 & 64+: $32,500 (+$8,000 catch-up)

Ages 60–63: $35,750 (+$11,250 SECURE 2.0 super catch-up)

$24,500 base

Ages 50–59 & 64+: $32,500 (+$8,000 catch-up)

Ages 60–63: $35,750 (+$11,250 SECURE 2.0 super catch-up)

Ages 50–59 & 64+: $65,000 (+$8,000 catch-up per account)

Ages 60–63: $71,500 (+$11,250 SECURE 2.0 super catch-up per account)

Want to keep these steps handy?

In 2007, I was $41,000 in debt, raising two kids as a single dad. I had a Chevy Trailblazer I could no longer afford. It was embarrassing, but my brother gave me his car, and my Dad drove it down to California from Washington. I remember dropping the Trailblazer keys off in the drop box at the bank and having it repossessed. I made a deal with the bank to pay off the remaining $14,000 — they lowered my payment to $250 a month during the payoff, and I paid back every penny. Once it was gone, that freed up about $500 a month. And on top of that, I went from a Trailblazer with terrible gas mileage to a Nissan Maxima that was far more efficient. The real monthly savings were even more than the car payment alone.

But I still had credit cards and other debt. Using the debt snowball method, I paid all of it off. I remember making that last payment so vividly. It was golden. I vowed to never let it happen again.

Life will test that vow — it tested mine. But the lesson isn't that you'll never take on debt again. The lesson is: if you do, have a plan to get out of it, and stick to it.

If I hadn't had that debt all those years, I could have been investing that money instead. Try your hardest to stay out of debt. Being debt-free is an amazing feeling.

“The best time to plant a tree was 20 years ago. The second best time is today.” — Chinese Proverb

💡 The Pre-Tax Benefit — What Contributions Actually Cost Your Paycheck

It's a common misconception that contributing $500/month means losing $500 from your take-home pay. It doesn't work that way.

Because 403(b) and 457(b) contributions come out before federal income taxes, the IRS lets you defer taxes on the money you contribute. At a 22% federal bracket, a $500/month contribution reduces your take-home pay by approximately $390/month — the other $110 represents federal tax you would have owed now but will pay later, in retirement, when you withdraw. If your state also has an income tax, your total deferral is larger (most states also exempt 403(b)/457(b) contributions from state income tax).

← Scroll to see full table →

*Based on 22% federal tax bracket only. State income tax deferral (where applicable) is additional. Nine states have no state income tax. Use the calculator below for numbers that reflect your specific bracket.

Important: Pre-tax contributions defer income taxes — they don't eliminate them. You'll owe income tax on these contributions and their growth when you withdraw in retirement. The benefit comes from compounding the full amount over time, plus potentially being in a lower tax bracket later.

Use the Paycheck Impact Calculator to see your exact numbers based on your own tax bracket and contribution amount.

💵 Try the Paycheck Impact Calculator

See exactly how pre-tax contributions affect your take-home pay based on your own tax bracket.

Try the Calculator →What This Looks Like on Your W-2

Here's how pre-tax 403(b) contributions show up on your actual W-2 form:

− 403(b): $6,000

= Box 1: $64,000

Making It Actually Happen: The Psychology of Saving

Knowing what to do and actually doing it are two different things. Here's how to make saving automatic and painless:

1. Pay Yourself First (Automate Everything)

Set up automatic contributions from your paycheck to your 403(b)/457(b). Many educators find that when contributions come out automatically, it's easier to stay consistent — you adjust to what lands in your paycheck. (See Coach Marty's story below.)

2. The "1% Every Year" Rule

Can't afford 10% right now? Start with 5%. Next year, bump it to 6%. The year after, 7%. By year 5, you're at 10%. By year 10, you might be maxing out. Small increases compound over time.

3. Save Half Your Raises

When you get your annual raise (or move up a step on the salary schedule), immediately increase your retirement contributions by half the raise amount. You still get a bump in take-home pay, but you also accelerate your savings.

Example: You get a $3,000 raise ($250/month). Consider increasing your 403(b) by $125/month. You keep $125 extra in your paycheck, but you just added $1,500/year to retirement savings.

4. Out of Sight, Out of Mind

Don't log into your retirement accounts every day. Check quarterly or annually. Market volatility will stress you out. Time in the market has historically outperformed timing the market.

5. The "Windfall Rule"

Tax refund? Bonus? Inheritance? Many educators choose to save at least half of any windfall and treat themselves with the rest. This accelerates your timeline without feeling like a sacrifice.

Remember the flexible deferral advantage from Module 2? This is exactly what it's built for — submit a one-time deferral election and funnel that windfall straight into your 457(b) before you can spend it.

Of all the tips above, "Pay Yourself First" is one that can't go unnoticed. I read David Bach's The Automatic Millionaire, and his concept was simple: automate your savings so the money never hits your checking account. You can't spend what you never see.

That's exactly what I did. I filled out my SRA form (I'll walk you through that in Module 8), set my 403(b) and 457(b) contributions to come straight out of my paycheck, and never looked back. No willpower required. No monthly decisions. Just automatic.

And this same principle works for a Roth IRA. Most brokerages — Fidelity, Vanguard, Schwab — let you set up automatic monthly transfers from your bank account directly into your Roth IRA. Pick a date, pick an amount, and it pulls every month without you lifting a finger. You're not hoping the money is there at the end of the month. It's gone before you can spend it.

Set it and forget it. Put that money to work. Many educators consider it one of the most powerful steps they can take.

Real Teacher Scenarios: What Would Coach Do?

Every teacher's situation is different — different salary, different debt, different timeline. Here's how I'd coach three teachers through the 6-step ladder based on where they are right now.

Scenario 1: Priya, First-Year Teacher Making $50,000

Situation: $20,000 in student loans at 5% interest, no emergency fund, living paycheck to paycheck.

Coach's Plan:

- Step 1: Build a 3-month emergency fund — even $50/paycheck gets her there

- Step 2: Student loans at 5% are typically considered moderate-interest — many financial educators suggest continuing minimum payments ($250/month) and moving on, since the long-term return on retirement contributions has historically exceeded that rate. Others may prefer paying loans down faster — both approaches have merit.

- Step 3a: If her district offers a 403(b) match (uncommon, but some districts do), contribute enough to grab the full match first

- Step 3: Open a Roth IRA with a low-cost provider (such as Fidelity or Vanguard, as examples) — start with even $100/month in a low-cost index fund

- As salary grows, add a 457(b) contribution, then increase 403(b) — follow the savings ladder from there

Why: Priya has 30+ years of compound growth ahead of her — time is her biggest asset. Student loans at 5% aren't an emergency. Many educators find that starting a Roth IRA early, even small, can be more impactful than waiting until the loans are paid off. The emergency fund keeps her from raiding retirement when life throws a curveball.

Scenario 2: Marcus, 15-Year Veteran Making $80,000

Situation: No retirement savings beyond pension, $10,000 credit card debt at 19% APR, kids in middle school.

Coach's Plan:

- Step 1: Build 3-month emergency fund as fast as possible

- Step 2: Many financial educators suggest prioritizing credit card debt at 19% APR — putting an aggressive amount toward it (for illustration, $800/month would eliminate it in about 14 months)

- Step 3: Open a Roth IRA and start contributing — he's been missing out on years of tax-free growth

- Step 4: Start 457(b) for early retirement flexibility — penalty-free access when he leaves his district

- Build toward 15% total savings rate as quickly as his budget allows

Why: At 19% APR, credit card interest can significantly erode any investment gains — which is why many financial educators suggest eliminating high-interest debt as a priority. Then he needs to catch up aggressively. He's missed 15 years of potential compound growth, but at $80K he has the salary to make a real dent if he follows the ladder.

Scenario 3: Jennifer, 20 Years In, Making $95,000

Situation: Contributing 5% to 403(b) for 10 years, no debt, solid emergency fund, wants to retire early at 55.

Coach's Plan:

Jennifer has already handled Steps 1 and 2. Time to accelerate through the rest of the ladder.

- Step 3: Max out her Roth IRA ($7,500/year) if she hasn't already — tax-free income in retirement

- Step 4: Max out 457(b) ($24,500/year) — accessible at 55 with no penalty, this can be a key tool for early retirement

- Step 5: Increase 403(b) beyond 5% — push toward maxing it

- Step 6: If she can swing it, max BOTH the 403(b) and 457(b) ($49,000/year total) — power saver mode

Why: Early retirement requires aggressive saving. The 457(b) is a key advantage because it's penalty-free before 59½. She has 15 years to catch up — time to go into power saver mode.

I had $41,000 in debt in 2007 and spent years climbing out of it before I ever invested a dollar. I didn't start investing until 52 — with zero in retirement accounts. If I can build a retirement I'm proud of from that starting point, you can absolutely do this from wherever you are right now.

The savings priority ladder is your roadmap. You don't have to do everything at once. Build the emergency fund, knock out the high-interest debt, open that Roth IRA, and start your 457(b) or 403(b). Every step forward is a step your future self will thank you for.

The only wrong move is not starting at all.